Latin America Precision Agriculture Market Statistics…

SOLAR TODO

Solar Energy & Infrastructure Expert Team

Watch the video

TL;DR

Latin America precision agriculture is expanding in 2026, led by Brazil and Argentina and supported by rising demand for weather, soil, and irrigation IoT. The strongest business case is usually on farms above 20 hectares, especially above 100 hectares, where LoRaWAN or 4G systems can deliver 15-30% water savings and typical payback in about 2-5 years.

Latin America precision agriculture is scaling in 2026, with Brazil and Argentina leading deployment. Most market models indicate roughly 10-15% CAGR, while weather-soil-irrigation systems on 20-100+ hectare farms often reach payback in 2-5 years.

Summary

Latin America precision agriculture is moving from pilot to scale in 2026, with connected-farm adoption still below North America but rising at double-digit rates. Brazil and Argentina lead deployment, while IoT, weather stations, and variable-rate irrigation show payback in roughly 2-5 years.

Key Takeaways

- Prioritize Brazil and Argentina, which account for the largest share of Latin America precision agriculture spending and the highest concentration of commercial farms above 100 hectares.

- Deploy IoT first on high-value crops and large blocks, where 10-minute data intervals and multi-point sensing can shorten response time by hours and improve irrigation control by 15-30%.

- Segment projects by farm size, because holdings above 100 hectares usually justify LoRaWAN or 4G field networks faster than farms below 20 hectares.

- Compare connectivity carefully: LoRaWAN can cover several kilometers at low power, while 4G LTE suits dispersed assets and higher data loads but raises annual operating cost.

- Use weather-plus-soil packages before adding AI crop diagnostics, because combined climate and root-zone data often deliver the fastest 2-4 year payback.

- Budget by delivery model: FOB supply is lowest upfront, CIF reduces logistics risk, and EPC turnkey improves commissioning control for projects above $1,000K.

- Verify standards and interoperability, including ISO 11783 data exchange, IP67/IP68 field protection, and utility-side compliance such as IEEE 1547 where power systems are involved.

- Ask suppliers for financing and staged rollout plans, because multi-zone deployments across 30-50 hectares can reduce water use by up to 50% in suitable applications.

Latin America Precision Agriculture Market Overview 2026

Latin America precision agriculture in 2026 is a mid-growth market led by Brazil and Argentina, with regional adoption commonly estimated in the low-to-mid teens of commercial farms and strongest demand in row crops, orchards, sugarcane, coffee, and export horticulture.

According to the Food and Agriculture Organization and national agricultural census patterns across the region, Latin America combines a high number of small farms below 20 hectares with a large share of agricultural output concentrated in medium and large commercial operations above 100 hectares. That structure matters because precision agriculture spending follows revenue concentration, machinery intensity, and irrigation exposure rather than farm count alone. In practice, the top 2 markets, Brazil and Argentina, account for a disproportionate share of connected-equipment, telematics, and digital agronomy spending in 2025-2026.

According to International Trade Administration country reporting and industry datasets from IICA, Brazil remains the largest precision agriculture market in the region due to its soybean, corn, sugarcane, cotton, and coffee base, while Argentina ranks second with strong adoption in large-scale grain operations. Mexico, Chile, Colombia, and Peru follow with stronger concentration in horticulture, vineyards, fruit, and irrigation-intensive crops. These segments use weather monitoring, soil probes, fertigation control, and disease-risk alerts more frequently than low-margin extensive grazing systems.

According to McKinsey and World Bank agriculture digitization studies published in recent years, digital agriculture adoption in Latin America still trails North America and Western Europe by a meaningful margin, but annual growth remains attractive because baseline penetration is lower. For B2B buyers, this means 2026 is less about replacing mature systems and more about first-time deployment, zone expansion, and integration of weather, soil, and irrigation data into one operating workflow.

Regional market snapshot

According to industry synthesis from IEA, IRENA, World Bank, and regional agritech trackers, precision agriculture demand is increasingly linked to three variables: water stress, export crop value, and farm consolidation. Water-intensive regions in Mexico, Peru, Chile, and Northeast Brazil show stronger demand for irrigation automation and evapotranspiration monitoring. Large mechanized belts in Brazil and Argentina show stronger demand for telematics, variable-rate application, and field connectivity.

| Region | 2026 market position | Main crops/use cases | Typical digital priority | Adoption profile |

|---|---|---|---|---|

| Brazil | Largest in Latin America | Soy, corn, sugarcane, coffee, citrus | Machinery data, weather, soil, irrigation | Highest absolute spend |

| Argentina | Second-largest | Soy, corn, wheat, sunflower | Variable-rate, telematics, climate risk | High on large farms |

| Mexico | Upper-mid tier | Berries, vegetables, avocado, citrus | Irrigation, fertigation, weather alerts | Strong in export zones |

| Chile | Mid tier | Vineyards, fruit, orchards | Frost, irrigation, disease control | High value per hectare |

| Colombia/Peru | Emerging-mid tier | Coffee, fruit, flowers, specialty crops | Microclimate, disease, water control | Fast growth from low base |

Market Statistics, Growth Rates, and Year-over-Year Trends

Latin America precision agriculture is widely tracked as a double-digit growth segment in 2025-2030, with most market models placing CAGR in roughly the 10-15% range depending on scope, hardware inclusion, and software definition.

According to Grand View Research and MarketsandMarkets category estimates for precision farming and smart agriculture, global precision agriculture growth remains above 10% CAGR through 2030, and Latin America generally grows near or slightly above the global average because installed base is smaller. According to Statista and regional agritech reporting, 2021-2024 growth was supported by high commodity prices, while 2025-2026 demand is more selective due to financing cost pressure and tighter farm margins in some crops.

A practical procurement view is to separate the market into 3 layers: sensing hardware, connectivity and gateways, and software analytics. Hardware usually dominates first-phase CAPEX in Latin America, especially where farms need weather stations, soil probes, solar-powered field nodes, and gateways. Software and advisory services grow later as farms move from monitoring to prescription and automation.

Historical to long-term trend analysis

According to IEA (2024), digitalization is becoming central to energy, water, and productivity management in agriculture, especially where diesel pumping and unstable grid supply raise operating costs. According to IRENA (2024), distributed renewables and digital controls are increasingly paired in rural applications, which supports solar-powered sensing nodes and autonomous field systems. This combination is particularly relevant in Latin America, where remote farms often face communication and power constraints at the same time.

| Period | Market trend in Latin America | Main demand driver | Buyer behavior |

|---|---|---|---|

| 2021-2022 | Recovery and pilot expansion | Commodity prices, export demand | Test projects and single-zone deployments |

| 2023-2024 | Faster digital trial activity | Water stress, labor shortages, input costs | More weather + soil packages |

| 2025-2026 | Selective scale-up | ROI discipline, irrigation efficiency, risk alerts | Focus on payback and interoperability |

| 2027-2030 | Broader automation growth | AI agronomy, machine data, compliance reporting | Multi-site integration and analytics |

| 2030-2040 | Platform consolidation | Autonomous operations, carbon and traceability data | Fewer vendors, deeper system integration |

According to BloombergNEF-style technology diffusion patterns across adjacent infrastructure markets, the 2030-2040 phase will likely reward suppliers that combine sensing, connectivity, and operational control rather than standalone devices. For buyers, this means system architecture in 2026 matters more than lowest unit price. A weather station without API access, ISO 11783 compatibility, or reliable field power can create replacement cost within 3-5 years.

Market size and growth comparison

According to multiple market trackers, exact values vary by definition, but the directional picture is consistent: Latin America is smaller than North America, Europe, and Asia-Pacific in total spend, yet it offers higher whitespace for first deployment.

| Region | 2026 estimated market maturity | Indicative 2025-2030 CAGR | Main constraint | Main opportunity |

|---|---|---|---|---|

| Asia-Pacific | High and broadening | 11-14% | Farm fragmentation in parts of Asia | Large-scale digital expansion |

| Europe | High and regulated | 9-12% | Compliance complexity | Sustainability-linked adoption |

| North America | Mature | 8-11% | Replacement cycle pressure | Analytics and autonomy |

| Middle East & Africa | Emerging | 12-16% | Water and financing constraints | Irrigation and remote monitoring |

| Latin America | Emerging-mid | 10-15% | Connectivity and CAPEX access | Large farms and export crops |

IoT Adoption by Farm Size and Crop Type

IoT adoption in Latin America is highest on farms above 100 hectares and in high-value irrigated crops, because larger blocks spread gateway cost and crops worth more than $3,000 per hectare can justify denser sensing.

According to FAO structural agriculture data and regional census patterns, most farms by count are small, but most marketed output often comes from a narrower group of medium and large enterprises. That is why adoption curves by farm count can look weak while revenue-weighted adoption looks much stronger. For procurement teams, the right question is not how many farms use IoT, but how much production area and crop value are digitally managed.

Large grain and sugar operations in Brazil and Argentina often begin with telematics, weather, and variable-rate application. Export fruit and orchard operators in Chile, Mexico, Peru, and Brazil often begin with frost alerts, irrigation scheduling, disease-risk monitoring, and fertigation control. Coffee and tea-like specialty systems in Colombia and some Andean zones rely more on microclimate variation, slope effects, and disease pressure, which makes distributed sensing valuable even on 20-50 hectare estates.

Farm size segmentation and likely adoption path

According to World Bank and IICA farm modernization studies, adoption economics improve materially once farms manage multiple zones, irrigation blocks, or geographically dispersed plots. A single gateway and 8-20 sensors can support a 30-50 hectare deployment, while a sub-10 hectare holding often needs cooperative models, service subscriptions, or government support to justify investment.

| Farm size | Typical adoption level in Latin America 2026 | Common technologies | Typical purchase trigger |

|---|---|---|---|

| 500 ha | Highest enterprise adoption | Integrated platforms, APIs, fleet + agronomy + energy | Scale, reporting, and centralized control |

Relevant system examples for Latin America buyers

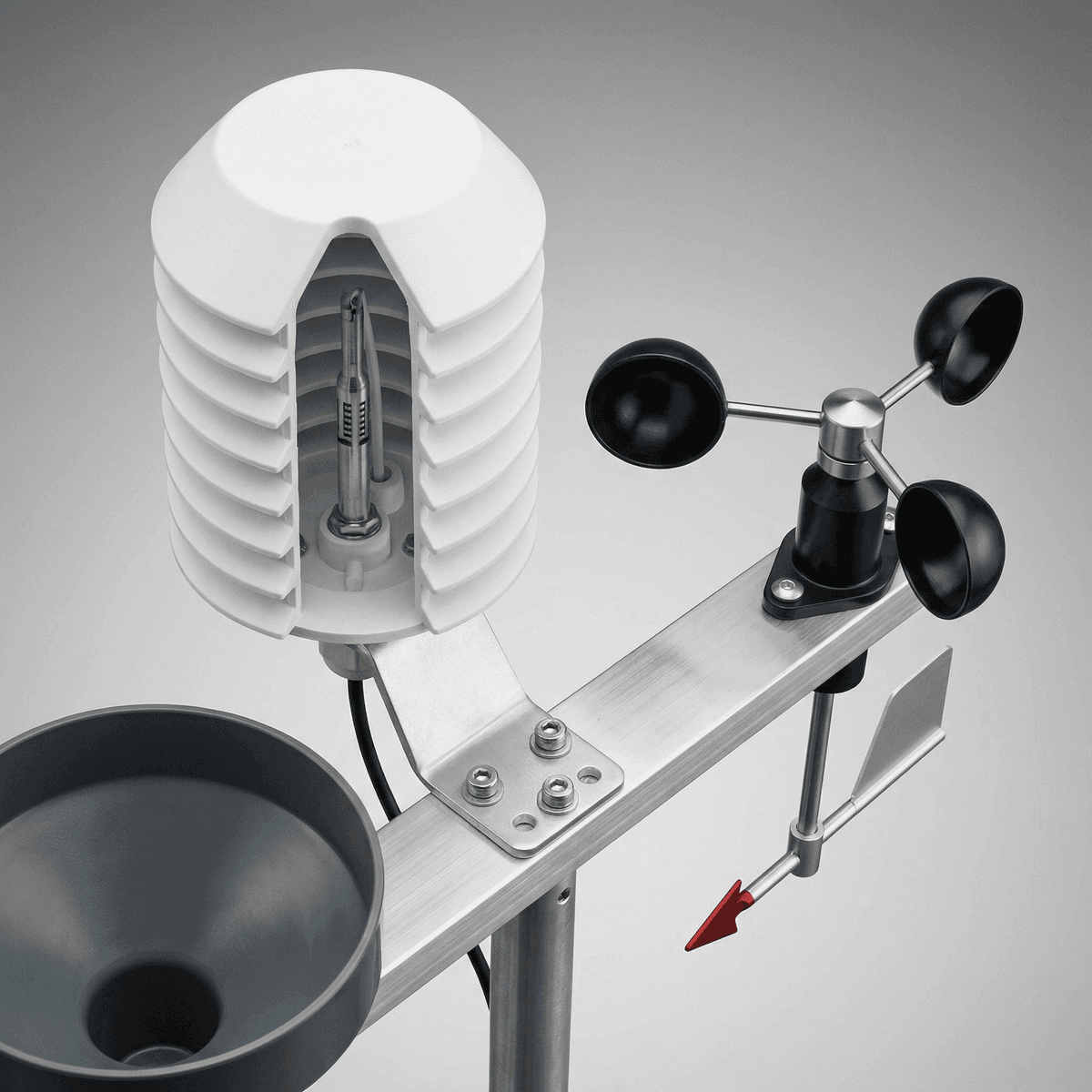

According to SOLAR TODO product configurations, a 30-hectare tea-style monitoring package uses 15 sensors/devices, 10-minute intervals, 1 cloud tier, and solar-powered LoRaWAN nodes. That architecture is relevant to Latin America specialty crops where elevation change, humidity, and fungal pressure vary across 10-500 meters. It is a good fit for estates that need microclimate visibility before disease symptoms become visible.

According to SOLAR TODO specifications, the Orchard Frost Early Warning 40ha package covers 40 hectares with 10 field sensing points, LoRaWAN communication, SMS plus Email plus App Push alerts, and wind machine control. For Chilean fruit, Mexican citrus, or Brazilian orchards, this layout matches frost-sensitive blocks where crop loss can occur within 1-3 hours when canopy temperature crosses critical thresholds near 0°C to -2.5°C.

According to SOLAR TODO specifications, the Desert Reclamation Solar+Agriculture 50ha package combines 500 kW solar PV, 20 sensors, 4G LTE, 10-parameter weather monitoring, 7-parameter soil analysis, and automated drip irrigation. While designed for desert reclamation, the architecture is also relevant to remote Latin American sites with unstable grid power, high evapotranspiration above 5-10 mm/day, and water-cost pressure.

Technology Stack, ROI Benchmarks, and EPC Investment Analysis and Pricing Structure

Precision agriculture ROI in Latin America is usually strongest when weather, soil moisture, and irrigation control are deployed together, with typical payback around 2-5 years depending on crop value, water cost, and area above 20 hectares.

According to NREL and IEA methodology used in energy-water project evaluation, ROI improves when systems reduce both resource use and operational uncertainty. In agriculture, that means fewer irrigation errors, earlier frost or disease response, and lower field inspection labor. According to sector studies cited by IRENA and World Bank, digital water management can reduce irrigation use by 15-30% in mainstream applications and by up to 50% in tightly managed drip systems under strong agronomic discipline.

A procurement-led specification should define 5 items before vendor comparison: coverage area in hectares, number of sensing points, communication type, data interval, and control outputs. For example, a 40-hectare orchard usually needs 8-10 field points if frost pockets vary by elevation, while a 30-hectare specialty crop may need 10-15 devices if disease pressure and moisture vary by slope and canopy density.

Connectivity and system comparison

According to field deployment practice, LoRaWAN suits low-power sensors over long distance, while 4G LTE suits mobile assets, dispersed sites, and higher bandwidth devices. IP67 or IP68 enclosure practice is standard for outdoor nodes, and ISO 11783 matters where farm machinery and data interoperability are part of the project scope.

| System type | Coverage example | Data interval | Connectivity | Best use case | Indicative payback |

|---|---|---|---|---|---|

| Weather + soil basic | 20-30 ha | 10-30 min | LoRaWAN | Irrigation scheduling | 2-4 years |

| Orchard frost warning | 40 ha | 10 min | LoRaWAN | Frost-sensitive fruit blocks | 1-3 seasons |

| Specialty crop disease monitoring | 30 ha | 10 min | LoRaWAN | Tea, coffee, vineyards, berries | 2-4 years |

| Solar + irrigation + soil | 50 ha | 10 min | 4G LTE | Remote high-ET farms | 3-5 years |

EPC Investment Analysis and Pricing Structure

EPC in this context means Engineering, Procurement, and Construction with commissioning, device configuration, cloud onboarding, and operator training included in one delivery scope. For projects above 30 hectares or with 10+ field devices, EPC reduces interface risk between civil works, power supply, communications, and software setup.

A three-tier pricing structure is standard for B2B buyers:

- FOB Supply: equipment only, ex-factory pricing, lowest upfront cost, best for buyers with local installers.

- CIF Delivered: equipment plus freight and insurance to destination port, useful where import logistics are complex.

- EPC Turnkey: supply, installation, testing, commissioning, and training, best for multi-zone farms and financed projects.

Volume pricing guidance commonly follows this structure:

- 50+ units or equivalent sensor-node volume: about 5% discount

- 100+ units: about 10% discount

- 250+ units: about 15% discount

Typical payment terms are:

- 30% T/T deposit and 70% against B/L

- 100% L/C at sight for qualified transactions

- Financing available for large projects above $1,000K

For project pricing, buyers should request 3 comparable offers with the same scope: hardware count, gateway count, cloud term, installation labor, and warranty period. For EPC and export inquiries, contact SOLAR TODO at [email protected] or +6585559114 for offline quotation and project review.

Regional Buyer Guidance and Supplier Selection Criteria

Brazil, Argentina, Mexico, Chile, and the Andean export corridor should be evaluated differently because farm structure, water stress, and crop value create different ROI thresholds and sensor density requirements.

Brazil and Argentina usually support larger deployments with stronger machinery integration and broader hectare coverage per project. Mexico, Chile, Peru, and Colombia often justify denser sensing per hectare because export fruit, vineyard, berry, and specialty crops have higher value and tighter quality windows. In practical terms, a 30-hectare orchard in Chile may justify more sensors than a 100-hectare grain block in Argentina because frost, disease, and irrigation timing have higher per-hectare financial impact.

Buyers should also compare energy architecture. Solar-powered field nodes reduce trenching and support remote deployment, while LFP-backed kits improve autonomy during poor weather or unstable grid conditions. According to IRENA (2024), distributed renewable systems continue to gain relevance in off-grid and weak-grid applications, which aligns with Latin American agricultural zones where reliable field power is not guaranteed.

Two authority statements are worth noting for procurement teams. The International Energy Agency states, "Digital technologies can improve energy efficiency, productivity and resilience across sectors," a point directly relevant to irrigation and remote farm operations. The International Renewable Energy Agency states, "Renewables are increasingly the most economic power option," which supports pairing solar supply with field monitoring and pumping control where diesel costs remain volatile.

Supplier due diligence should cover:

- Coverage proof in hectares and number of field nodes

- Data interval, usually 10 minutes for active agronomy decisions

- Alert methods such as SMS, Email, and App Push

- API access and export format compatibility

- IP67/IP68 outdoor protection and warranty term

- Local installation support and spare parts lead time

FAQ

A practical 2026 benchmark is that Latin America remains smaller than North America in precision agriculture spend, but it is growing at roughly 10-15% CAGR in many market models. Brazil and Argentina lead by scale, while Mexico, Chile, Peru, and Colombia show strong adoption in high-value irrigated and export crops.

Q: What is driving precision agriculture growth in Latin America in 2026? A: Water stress, labor cost pressure, and export quality requirements are the main drivers in 2026. Farms are adopting weather stations, soil probes, and irrigation controls because these tools can reduce water use by 15-30% and improve response time to frost or disease by hours rather than days.

Q: Which Latin American countries lead IoT adoption in agriculture? A: Brazil leads in absolute market size, and Argentina ranks second for large-scale commercial adoption. Mexico, Chile, Peru, and Colombia are also important because high-value fruit, vineyard, coffee, and horticulture crops justify denser sensing and faster payback per hectare.

Q: How does farm size affect IoT adoption rates? A: Farm size matters because gateway, cloud, and installation costs spread more efficiently across larger areas. Holdings above 100 hectares usually justify LoRaWAN or 4G systems faster, while farms below 20 hectares often need cooperative purchasing, service subscriptions, or subsidy support.

Q: What technologies are most commonly deployed first? A: The first deployment is usually weather monitoring plus soil moisture and temperature sensing at 10-minute intervals. These systems address irrigation timing, frost risk, and disease pressure with lower complexity than full variable-rate or AI prescription platforms, so payback often arrives within 2-4 years.

Q: Is LoRaWAN or 4G LTE better for agricultural IoT projects? A: LoRaWAN is usually better for low-power sensors across several kilometers, especially on 20-50 hectare blocks. 4G LTE works better for dispersed sites, mobile assets, and larger data loads, but annual connectivity cost is higher and power demand is less forgiving.

Q: What payback period should buyers expect in Latin America? A: Many projects target a 2-5 year payback, but the range depends on crop value, irrigation intensity, and labor cost. Frost-warning systems in orchards can pay back in 1-3 seasons if one avoided damage event protects blossoms or young fruit on a 30-40 hectare block.

Q: How should buyers evaluate systems by crop type? A: Grain and sugar operations usually prioritize telematics, weather, and variable-rate tools over dense biological sensing. Orchards, vineyards, berries, coffee, and specialty crops usually prioritize microclimate, soil moisture, disease alerts, and irrigation control because quality and yield losses occur faster and cost more per hectare.

Q: What standards and technical specifications should be checked? A: Buyers should check ISO 11783 for agricultural data interoperability where machinery data is involved, plus IP67 or IP68 protection for outdoor devices. If the project includes solar power, pumps, or grid-tied electrical systems, IEEE 1547 and relevant IEC electrical standards should also be reviewed.

Q: What does EPC turnkey delivery include for smart agriculture projects? A: EPC turnkey delivery usually includes engineering review, equipment supply, installation, commissioning, cloud setup, and operator training. It is useful for projects above 30 hectares or with 10+ devices because it reduces coordination gaps between civil works, communications, power systems, and software onboarding.

Q: What are typical pricing and payment terms for B2B buyers? A: Pricing is commonly structured as FOB Supply, CIF Delivered, or EPC Turnkey depending on project scope and local installation capability. Standard payment terms are often 30% T/T and 70% against B/L, or 100% L/C at sight, with financing available for projects above $1,000K.

Q: How can SOLAR TODO support Latin America projects? A: SOLAR TODO supplies smart agriculture monitoring systems for 30-hectare, 40-hectare, and 50-hectare use cases with LoRaWAN or 4G architectures. The company supports offline quotation, export delivery, and project financing review, which is useful for buyers planning phased deployment across multiple zones.

Conclusion

Latin America precision agriculture in 2026 is a growth market where the strongest ROI usually comes from weather, soil, and irrigation control on farms above 20 hectares and especially above 100 hectares. For buyers comparing suppliers, SOLAR TODO offers practical 30-50 hectare architectures with 10-minute monitoring, LoRaWAN or 4G connectivity, and EPC options that fit phased regional deployment.

References

- IEA (2024): Energy Technology Perspectives and digitalization guidance relevant to agricultural energy, monitoring, and efficiency.

- IRENA (2024): Renewable Capacity Statistics and rural energy transition findings relevant to solar-powered field systems.

- NREL (2024): Distributed energy and performance modeling methodologies applicable to solar-powered agricultural monitoring and pumping.

- FAO (2023): Agricultural structure and farm-size datasets used to assess smallholder concentration and production distribution.

- World Bank (2024): Agriculture digitalization, water productivity, and climate resilience analysis across emerging markets.

- IICA (2024): Regional agriculture modernization and digital transformation reporting for Latin America.

- IEEE 1547-2018 (2018): Standard for interconnection and interoperability of distributed energy resources with electric power systems.

- ISO 11783 (2023): Agricultural machinery and data communication standard for interoperability across digital farming systems.

About SOLARTODO

SOLARTODO is a global integrated solution provider specializing in solar power generation systems, energy-storage products, smart street-lighting and solar street-lighting, intelligent security & IoT linkage systems, power transmission towers, telecom communication towers, and smart-agriculture solutions for worldwide B2B customers.

About the Author

SOLAR TODO

Solar Energy & Infrastructure Expert Team

SOLAR TODO is a professional supplier of solar energy, energy storage, smart lighting, smart agriculture, security systems, communication towers, and power tower equipment.

Our technical team has over 15 years of experience in renewable energy and infrastructure, providing high-quality products and solutions to B2B customers worldwide.

Expertise: PV system design, energy storage optimization, smart lighting integration, smart agriculture monitoring, security system integration, communication and power tower supply.

Cite This Article

SOLAR TODO. (2026). Latin America Precision Agriculture Market Statistics…. SOLAR TODO. Retrieved from https://solartodo.com/knowledge/latin-america-precision-agriculture-market-statistics-2026-iot-adoption-farm-size-data

@article{solartodo_latin_america_precision_agriculture_market_statistics_2026_iot_adoption_farm_size_data,

title = {Latin America Precision Agriculture Market Statistics…},

author = {SOLAR TODO},

journal = {SOLAR TODO Knowledge Base},

year = {2026},

url = {https://solartodo.com/knowledge/latin-america-precision-agriculture-market-statistics-2026-iot-adoption-farm-size-data},

note = {Accessed: 2026-05-03}

}Published: May 3, 2026 | Available at: https://solartodo.com/knowledge/latin-america-precision-agriculture-market-statistics-2026-iot-adoption-farm-size-data

Subscribe to Our Newsletter

Get the latest solar energy news and insights delivered to your inbox.

View All Articles